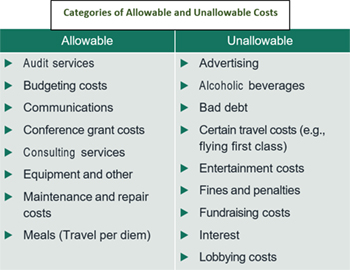

We briefly discussed allowable costs in the article “The Fantastic Four,” which identified cost allowability as one of the four most common single audit findings. Basic financial management cost principles define any charges incurred by the federal grant as either allowable or unallowable. Allowable costs are charges incurred by a program that can be covered with your federal grant. Unallowable costs are charges incurred by a program that cannot be covered or reimbursed by your federal grant.

What You Need to Know

Allowable costs (for all non-federal entities, other than for-profit entities and hospitals) are those costs consistent with the principles set out in 2 CFR 200, Subpart E, and those permitted by the grant program’s authorizing legislation. The fact that a cost requested in a budget is awarded does not ensure a determination of allowability. The organization is responsible for consistently presenting costs. To be allowable (see 2 CFR 200.403), a cost charged to an award must be:

- Allocable to the award under the provisions of the applicable cost principles;

- Necessary and reasonable for proper and efficient performance and administration of the grant or cooperative agreement;

- Treated consistently as direct or indirect costs;

- Adequately document; and,

- Consistent with the recipient’s policies, regulations, and procedures that apply to federal awards and other activities of the recipient.

Unallowable costs are costs that cannot meet the criteria of reasonableness, allowability, allocability, and consistency. Non-federal entities must not use award or match funding for unallowable costs. Also, any costs considered inappropriate by the awarding agency are within the category of unallowable costs. For a cost to be unallowable, it will be one or all of the following:

- Unreasonable or unallocable;

- Limited or excluded by Federal Cost Principles or other laws and regulations;

- Inadequate Documentation. The documentation must be able to support the expenditures; and,

- Prohibited costs such as conflicts of interest in procurements.

Best Practices for Avoiding Unallowable Costs

As a recipient of federal funds, you do not want to incur costs that won’t be reimbursed. So here are a few tips to help you avoid incurring unallowable expenses.

- Implement an adequate and comprehensive compliant accounting system that can track allowable and unallowable costs as they are entered into the system.

- Develop formal written policies and procedures for your entire organization that describe allowable and unallowable costs.

- Train key personnel on these policies and procedures.

- Test the policies and procedures frequently to ensure they are operating effectively. This can be done via internal audits.

- Review and revise your policies and procedures to ensure they are in compliance.

If you are unsure whether a cost is allowable or unallowable, always reach out to your Federal program manager or grants specialist. Allow them to make the final determination as to whether or not a cost is allowable or unallowable. Remember this, if you wouldn’t use your own money to incur this particular cost, you shouldn’t use federal dollars to incur that cost.

Resources

CFR 200, Subpart E